Credit score:

A credit score is a numerical representation of your creditworthiness. It’s calculated based on your credit history, including factors like your payment history, credit utilisation, length of credit history, and more. Lenders use your credit score to assess the risk of lending to you. A higher credit score typically means better loan terms and lower interest rates, while a lower score might result in less favourable terms or loan denials. It’s crucial to monitor and maintain a good credit score to access affordable loans and financial opportunities.

Difference between fixed-rate and variable-rate loans:

Fixed-rate loans have a constant interest rate throughout the loan term, providing predictable monthly payments. Variable-rate loans, also known as adjustable-rate loans, have interest rates that can change periodically, typically tied to a benchmark index. Fixed-rate loans offer stability, while variable-rate loans may start with lower rates but come with the risk of higher payments if rates rise. The choice depends on your risk tolerance and market conditions

Why Choose a Mortgage Broker Over a Bank Loan?

You might opt to engage a mortgage broker rather than approaching a bank directly because brokers offer several valuable benefits. These independent professionals have access to numerous lenders and loan products, including those from banks, potentially providing you with more favourable terms and rates. Mortgage brokers simplify the loan shopping process, saving you time and effort by researching and comparing various lender offers. They also offer expert advice tailored to your financial situation and goals, helping you navigate complex mortgage terms and conditions. Additionally, brokers may negotiate with lenders on your behalf to secure better terms and can be particularly helpful if you have unique financial circumstances or credit challenges. Their flexibility and convenience in scheduling meetings make the application process smoother. While banks are a valid option, working with a mortgage broker can enhance your choices and provide expert guidance to find the best mortgage for your specific needs.

Reclaim Excess Funds: SMSF Overpayment Withdrawal

Contributions generally cannot be returned to a member because:

- they regret making the contribution.

- they or their agents made an error in their decision to contribute.

Contributions may only be refunded in circumstances tightly prescribed by legislation.

Empty Home Revival: Selling After 6 Years – Unleash CGT

If you are not treating any other property as your Principal Place of Residence (PPOR), you can continue to treat this property as your primary residence indefinitely after you have stopped residing in it.

Empower Your Quest: CGT Concession in Small Business

You are considered a CGT Concession Stakeholder in a company or trust if you are:

- A significant individual in that company or trust.

- The spouse of a significant individual and have a small but more than zero percent stake in the company or trust.

You can own this stake either directly or through other entities. To calculate your stake, use the same method as the significant individual test.

You’re a significant individual in a company or trust if you own at least 20% of it. This 20% can include both your direct ownership and indirect ownership through other entities.

Special Note – A spouse of a significant individual must have a participation percentage greater than zero in the business entity.

Small Business CGT Concession and Roll-Over Rules:

CGT Event J5 occurs if, after choosing a roll-over for a capital gain, you haven’t acquired a new asset or improved an existing one by the end of the allotted time. Additionally, this event happens if:

- The new or improved asset isn’t actively used in your business anymore (like if you’ve sold it, it’s now part of your trading stock, or it’s no longer used in your business operations).

- If the new asset is a share in a company or a trust interest, and it fails the 80% test (unless this failure is only temporary).

- You or a related entity aren’t significant stakeholders in the company or trust.

- The stakeholders in the company or trust don’t have a significant (at least 90%) investment in your business. When CGT Event J5 happens, you’ll have to recognize a capital gain. This is the same amount you initially didn’t have to pay tax on because of the small business roll-over. The capital gain is counted at the end of the time you were supposed to get or improve the asset.

Example: CGT event J5

In September 2020, Luke made a capital gain of $80,000 on an active asset. He met the maximum net asset value test.

Luke disregarded the whole capital gain under the small business roll-over.

In September 2022 (the end of the 2-year period), Luke did not have any replacement or capital improved assets. CGT event J5 happens, and Luke makes a capital gain of $80,000 in September 2022.

Source – ATO/ Small Business Rollover

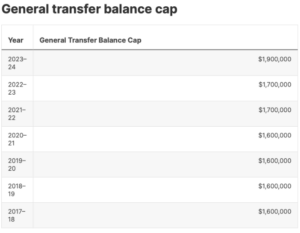

General Transfer Balance Cap in 2024

Source: ATO/General Transfer Balance Cap

In the context of your Self-Managed Superfund (SMSF), your transfer balance cap represents the upper limit on the total amount of accumulated superannuation funds you

can move into retirement phase accounts, which enjoy tax-free earnings. This cap is not a one-time figure; it’s a lifetime limit that applies to all transfers you make over the course of

your life into retirement phase pensions.

With the commencement of your retirement phase income stream within your SMSF, your personal transfer balance cap will be equivalent to the prevailing general transfer balance

cap at that juncture.

Please note that since the 1st of July 2021, the general transfer balance cap is indexed with inflation, tracked by the consumer price index, and is adjusted in $100,000 increments. This

indexation can potentially increase your transfer balance cap over time, enhancing the amount you can shift into your SMSF retirement phase account, thereby maximizing your

superannuation’s tax-effective potential.

Source: ATO – Transfer Balance Cap Explanation